It is crucial to recognise that the ongoing shift in peripheral MMR is not merely a connectivity story. It represents a strategic inflection point for the region’s next phase of urban expansion. The commissioning of the Atal Setu and the fast-tracked development of the Navi Mumbai International Airport has fundamentally reshaped the real estate narrative. Travel time between Sewri and Navi Mumbai has been reduced to less than 25 minutes, prompting a decisive response from both investors and end-users. Residential activity across Panvel, Ulwe and surrounding micro-markets has accelerated sharply. The critical question, however, remains: does this signal authentic decentralisation, or is it primarily infrastructure-led optimism driving the momentum?

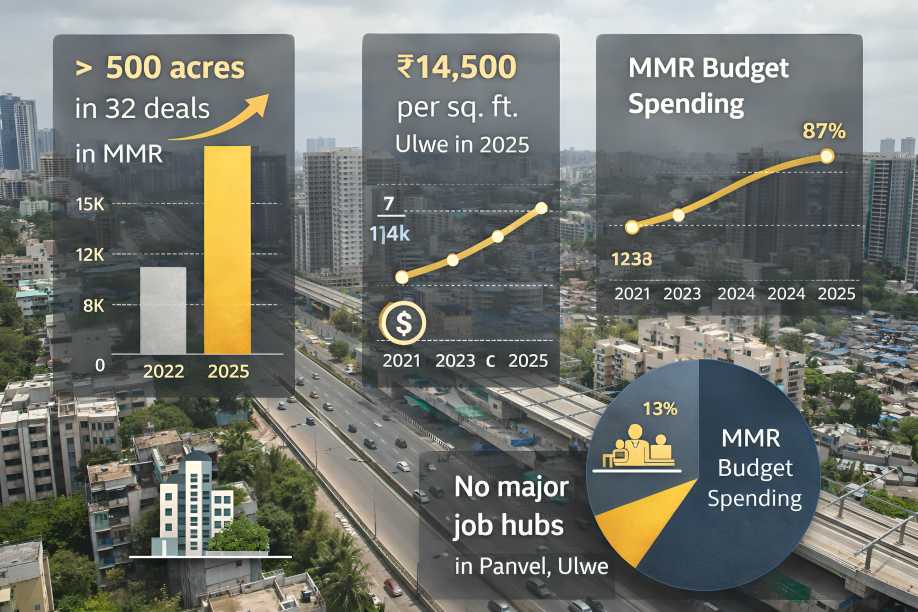

Infrastructure remains the undeniable driver. Transaction data shows that in 2025, over 500 acres of land were transacted across 32 deals in the MMR, making it one of India’s most active land markets. Developers are positioning for growth around airport influence zones and key highway corridors. The MMRDA’s Rs 48,073 crore budget for 2026–27 dedicates nearly 87% to infrastructure, including transformative projects such as the proposed Rs 4,000 crore “Mumbai 3.0” town centre. On paper, this scale of capital allocation signals intent. In practice, it will only translate into sustained growth if transport links, employment clusters, and social infrastructure evolve simultaneously.

Transport improvements define opportunity. The Atal Setu, new expressways, and upgraded arterial roads are game-changers for travel time and accessibility. But connectivity alone does not make self-sustaining cities. Without corresponding development of employment hubs, healthcare facilities, and education infrastructure, Panvel and Ulwe risk becoming commuter extensions rather than vibrant satellite nodes. Residential markets may heat up, but price appreciation without local job creation could inflate speculative bubbles.

Real estate economics in peripheral MMR will also depend on municipal and regional fiscal strategies. Higher premiums, revised development rights, and regulatory adjustments are tools to fund infrastructure, yet they increase project costs. Unless approvals are streamlined, and road, airport, and link-road projects are executed efficiently, these measures may pass on input costs to end-users. In other words, infrastructure can unlock value—but only if delivery aligns with planning intent.

Employment and social infrastructure remain the missing puzzle pieces. Airoli and Vashi have established business and IT clusters, yet Panvel and Ulwe largely rely on future potential. Grade-A office space absorption, healthcare hubs, and educational institutions must expand alongside housing. Otherwise, improved transport merely lengthens daily commutes without redistributing economic activity. Housing-led expansion cannot substitute for holistic urbanisation.

The takeaway is clear: peripheral MMR’s real estate trajectory will be decided not by sentiment or short-term price gains, but by infrastructure credibility and sequencing. Bridges, airports, and highways create expectations, but only synchronized execution of civic, social, and commercial facilities will transform these regions into true satellite cities. Otherwise, the region may simply be redrawing commuting maps rather than building self-sustaining urban ecosystems.

In essence, the Atal Setu and the airport are catalysts, not outcomes. Peripheral MMR has potential, but ambition must translate into delivery. The next real estate cycle will hinge on whether infrastructure investment enhances livability, not just connectivity.