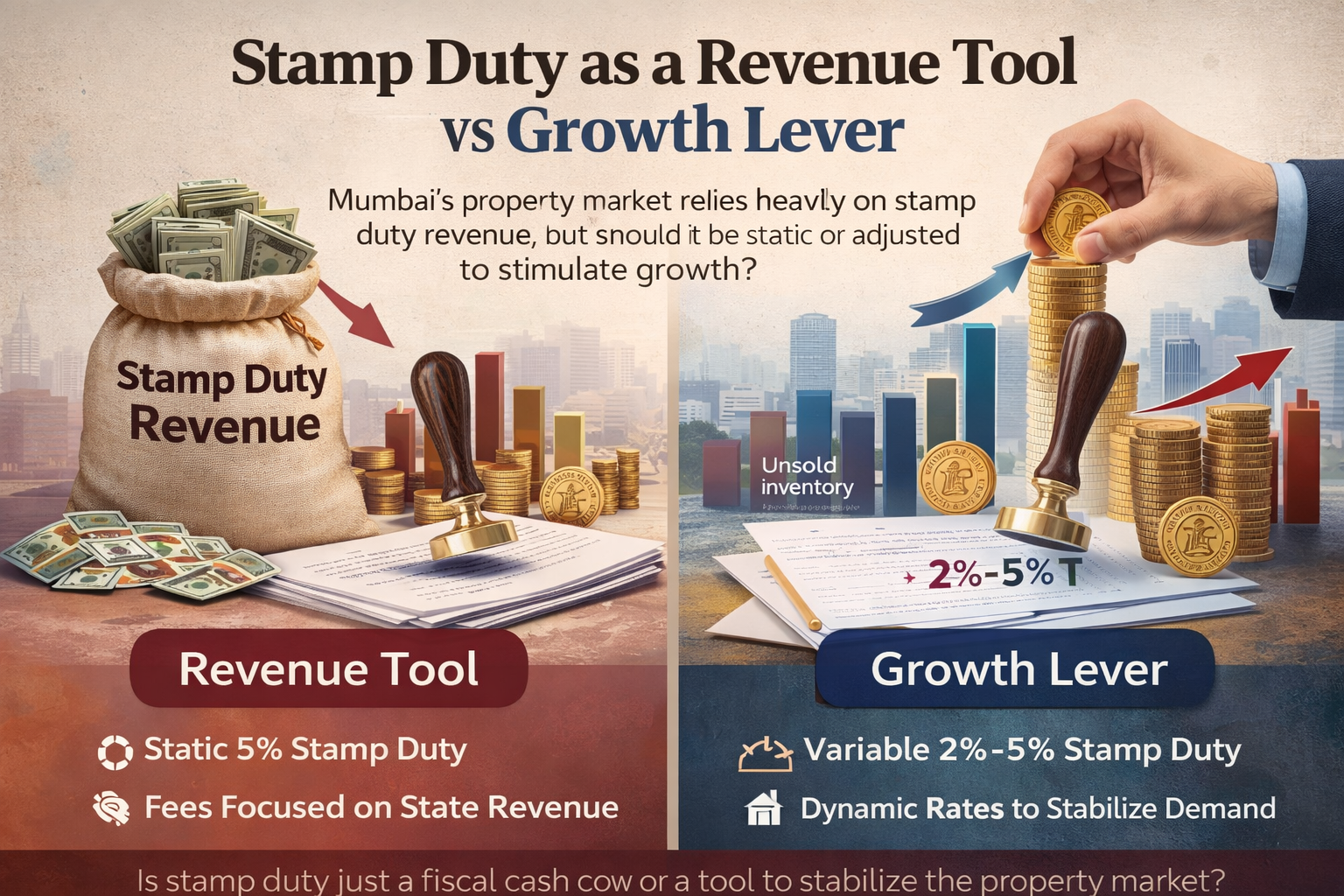

If stamp duty remains merely a fiscal cash cow, the property market will continue to move in volatile cycles. But used strategically, it could become a powerful lever to stimulate demand, stabilise transactions and sustain long-term market growth.

In Maharashtra, stamp duty on property transactions has long been one of the state government’s most dependable sources of revenue. Every property registration contributes significantly to public finances, particularly in Mumbai where real estate prices are among the highest in the country. However, the discussion around stamp duty is gradually shifting. Instead of treating it purely as a revenue-generating tax, policymakers and market observers are beginning to consider whether it can also be used to support and stabilise the property market.

The pandemic period provides an important example. In 2020, the Maharashtra government temporarily reduced stamp duty in Mumbai from 5% to 2% between September and December, before increasing it to 3% until March 2021. The impact on the market was immediate. Lower transaction costs encouraged buyers to enter the market, and property registrations rose sharply during this period.

Data from the Inspector General of Registration and Stamps shows, that Mumbai recorded more than 1.5 lakh property registrations in FY2025, one of the highest annual figures in nearly a decade. During the concession period, monthly registrations crossed 10,000 transactions per month several times, compared with fewer than 5,000 per month earlier in the pandemic. Despite the reduced rates, the state still collected more than Rs 9,000 crore in stamp duty revenue that year, as the rise in transaction volumes made up for the lower tax rate.

This clearly shows that stamp duty influences market behaviour. Property purchases involve significant upfront expenses, and transaction taxes form a major part of that cost.

In Mumbai, stamp duty and registration charges together generally add around 6–7% to the total cost of a property. For a home priced at Rs 1.5 crore, this means an additional Rs 9–10 lakh in charges at the time of purchase. For many buyers, particularly first-time homebuyers, this becomes a major financial hurdle. Even a small reduction in these costs can make a noticeable difference to purchasing decisions.

This is why a more flexible approach to stamp duty deserves consideration. Instead of keeping rates fixed regardless of market conditions, they could be adjusted in response to indicators such as unsold housing inventory, demand cycles and affordability levels.

For example, if unsold housing inventory increases significantly across the Mumbai Metropolitan Region, a temporary reduction in stamp duty could help stimulate demand and support faster sales. On the other hand, during periods of excessive speculation or rapidly rising prices, slightly higher transaction taxes could help moderate demand.

Such an approach could improve both market stability and government revenue. Real estate is a volume-driven sector, and higher transaction activity benefits several related industries, including construction, housing finance, home furnishings and consumer spending.

The wider economic impact is substantial. According to estimates by the National Real Estate Development Council, the real estate sector currently contributes around 7% to India’s GDP and is expected to reach nearly 13% by 2030. Policies that help maintain steady transaction cycles can therefore have broader economic benefits.

Importantly, a dynamic stamp duty policy does not necessarily reduce government revenue. The temporary stamp duty cut during the pandemic demonstrated that lower transaction costs can draw more buyers into the market, increasing the number of registrations and often compensating for the reduced tax rate through higher overall volumes.

Ultimately, stamp duty will always remain an important source of revenue for the state. The larger question is whether it should also be used as a policy tool to support the property market.

In a city as economically important as Mumbai, treating property transactions only as a steady revenue stream may not be the most effective approach. A carefully calibrated stamp duty policy could turn the tax into a growth lever, encouraging transactions, improving affordability and helping the housing market remain stable rather than moving through repeated cycles of slowdown and surge.